What Is Insurance and How Does It Work?

What Is Insurance and How Does It Work?

What Is Insurance and How Does It Work?

Insurance is a financial arrangement that helps protect individuals and businesses from unexpected losses.

By paying a small amount regularly, known as a premium, policyholders receive financial support when certain

unplanned events occur, such as accidents, illness, property damage, or death.

The main purpose of insurance is to reduce financial risk and provide peace of mind. Instead of bearing the full

cost of a loss alone, insurance spreads the risk among many people.

Why Insurance Is Important

Life is unpredictable, and unexpected events can lead to serious financial difficulties. Insurance helps

individuals and families manage these risks effectively.

- It protects savings from being wiped out by emergencies

- It helps cover medical and healthcare expenses

- It provides financial support to dependents

- It safeguards property and valuable assets

Without insurance, even a minor accident or illness could create long-term financial stress.

How Insurance Works

Insurance works on the principle of risk pooling. Many people contribute premiums into a shared fund managed

by an insurance company. When a policyholder experiences a covered loss, compensation is paid from this fund.

The process typically involves the following steps:

- Choosing an insurance policy

- Paying regular premiums

- Filing a claim when a covered event occurs

- Receiving compensation after claim approval

Common Insurance Terms Explained

Understanding basic insurance terms helps policyholders make better decisions.

- Premium: The amount paid regularly to keep the policy active

- Policy: The contract between the insurer and the policyholder

- Coverage: The protection provided by the insurance

- Deductible: The amount paid by the policyholder before insurance applies

- Claim: A request for compensation after a loss

Types of Insurance Everyone Should Know

There are many types of insurance designed to meet different needs. The most common include:

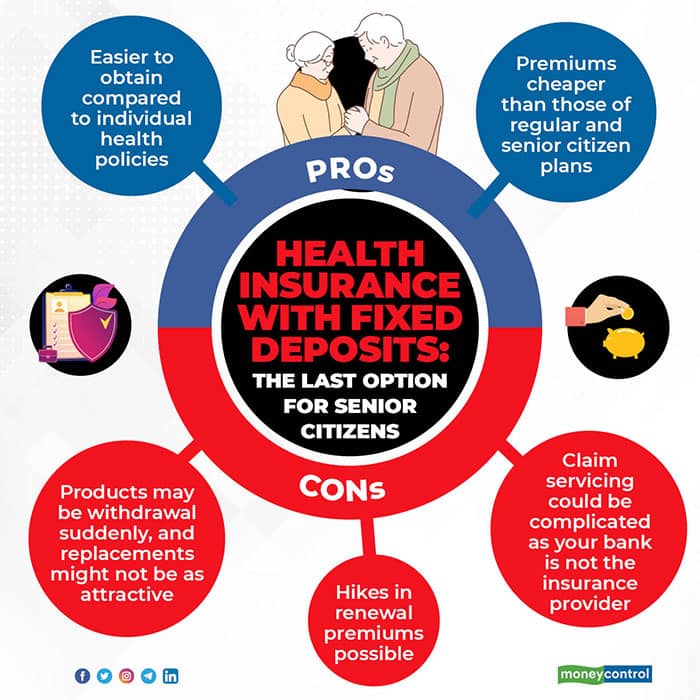

Health Insurance

Health insurance covers medical expenses such as doctor visits, hospital stays, medications, and preventive care.

It helps reduce the financial burden of healthcare costs.

Life Insurance

Life insurance provides financial support to beneficiaries after the policyholder’s death. It is often used to

cover funeral costs, debts, and daily living expenses for family members.

Car Insurance

Car insurance protects against losses related to vehicle damage, theft, and liability from accidents. In many

countries, it is legally required.

Home Insurance

Home insurance covers damage to property and personal belongings caused by events like fire, theft, or natural disasters.

Travel Insurance

Travel insurance offers protection against trip cancellations, medical emergencies, and lost luggage while traveling.

How Insurance Claims Work

An insurance claim is a formal request made to an insurance company for compensation. Once a claim is submitted,

the insurer reviews the details to ensure the loss is covered under the policy.

If approved, payment is made according to the policy terms. Claims may be denied if policy conditions are not met

or required documentation is missing.

Common Insurance Mistakes to Avoid

- Not reading policy documents carefully

- Choosing coverage based only on price

- Failing to update policies when life changes

- Ignoring policy exclusions

Avoiding these mistakes can help ensure better protection and smoother claim processing.

How to Choose the Right Insurance Policy

Selecting the right insurance policy requires careful consideration of personal needs, financial situation, and

risk exposure. Comparing policies, understanding coverage limits, and reviewing exclusions are essential steps.

It is also important to choose reputable insurance providers with good customer service and claim settlement records.

Conclusion

Insurance plays a vital role in financial planning by providing protection against unexpected events. Understanding

how insurance works, the types available, and common terms helps individuals make informed decisions.

By choosing the right insurance coverage, individuals can safeguard their health, assets, and financial future

with confidence.

:max_bytes(150000):strip_icc()/dotdash-hsa-vs-fsa-v3-66871b956baa4be786d2138777e70067.jpg)